Feedback on the input provided by the European Parliament as part of its resolution on the ECB’s Annual Report 2022

This feedback statement is being published on the occasion of the ECB’s Annual Report 2023 being presented to the European Parliament. It provides responses to the issues raised and requests made by the European Parliament in its resolution on the previous year’s ECB Annual Report.[1] The statement is structured by topic. It serves to better explain the ECB’s policies and promote dialogue with the European Parliament and the public regarding the important issues highlighted by the Members of the European Parliament.[2] The ECB has been publishing such feedback statements since 2016, following a suggestion by the European Parliament.

1 Monetary policy and economic developments

As regards the call to take all necessary measures to reduce the inflation rate in accordance with its mandate, the ECB is determined to ensure that inflation returns to its 2% medium-term target in a timely manner. The ECB has taken several steps to that end. Most prominently it raised its key policy rates by as much as 450 basis points between July 2022 and September 2023. The ECB had already started normalising its monetary policy in December 2021, by announcing the phasing-out of some of its asset purchases. Incoming information in the first half of 2022, characterised by an exceptional degree of uncertainty, gradually confirmed that inflation was likely to stay too high for longer than initially anticipated. Since then, the ECB has raised the policy interest rates at a speed and on a scale that are unprecedented. In any case an earlier start of the hiking cycle would likely have had only a limited impact on inflation in the near term and over longer horizons. Economic and financial conditions differ between economic areas. Comparisons with monetary policy reactions in other jurisdictions, notably the United States, should therefore be treated with caution. Going forward, future decisions will ensure that policy rates will be set at sufficiently restrictive levels for as long as necessary, based on a data-dependent approach. The ECB’s monetary policy, by stabilising inflation at the medium-term 2% target, contributes to sustainable economic growth and job creation. Moreover, price stability-oriented monetary policy also helps limit the inequality fuelled by high inflation. Lower-income households are generally affected more by inflation as they spend a higher proportion of their income and have lower financial buffers.

On concerns about second-round effects, an unanchoring of inflation expectations, and the possibility of a wage-price spiral, recent data imply that the risk of such effects materialising has diminished and remains contained. Recent data provide evidence of ongoing disinflation and an emerging moderation of wage growth. Wage bargaining aimed at inflation compensation implies some second-round effects, but this has not led to a self-sustaining spiral. Such a risk naturally increases according to how long and by how much inflation deviates from the 2% target. But inflation has come down strongly and is projected to reach the target in mid-2025. This partly reflects the forceful monetary policy action taken by the ECB. When assessing its monetary policy stance, the ECB continues to monitor the pass-through of inflation to all relevant real and nominal variables, to ensure that inflation returns to its 2% medium-term target in a timely manner. Both the long-term inflation expectations of professional forecasters and market-based measures have remained anchored around the 2% inflation target, with consumer expectations slightly elevated. The ECB continues to monitor these developments carefully.

On the request to provide more information with regard to the monitoring and setting of the neutral interest rate, such a rate is unobservable and its estimation is subject to a host of measurement and model-specification challenges. The neutral interest rate is defined as the interest rate that is neither expansionary not contractionary. ECB staff use a range of estimates to gauge the level of and developments in the neutral rate. Cyclical measures of the neutral rate in the euro area appear to have risen since the COVID-19 pandemic. However, slow-moving estimates anchored to long-run economic trends are unlikely to have increased much in the absence of changes in structural economic drivers (productivity growth, demographics and risk aversion). Earlier this year ECB staff published more information on the uses and limitations of the neutral rate of interest.[3] It should be noted that central banks only estimate – and do not set – neutral interest rates.

With regard to the meaning of “medium term” in the inflation target and looking into a more qualitative approach to price stability, no numerically precise ex ante definition of “medium term” exists, while a precise numerical target for headline inflation is instrumental in anchoring inflation expectations. This was explained, for example, in the ECB’s previous feedback statement.[4] The medium-term orientation allows for inevitable short-term deviations of inflation from the 2% target. It also takes into account lags and variability in the transmission of monetary policy to the economy and inflation. The length of the medium term varies according to conditions such as the origin, magnitude and persistence of the deviation of inflation from target. Regarding the definition of the inflation target, the 2021 strategy review concluded that price stability is best maintained by aiming for a symmetric 2% inflation target over the medium term.[5] Having such a quantitative target provides a clear anchor for inflation expectations, which is essential for maintaining price stability. In fact, most inflation expectations have remained broadly anchored around 2%, despite the recent episode of very high inflation rates. This shows that the ECB’s target is well understood and credible.

Regarding the request to fundamentally review and improve the ECB models used for monetary policy preparation, it is important to emphasise that the ECB constantly revises and updates its models.[6] The ECB uses a wide range of models for its projections. These models utilise information from empirical patterns observed in the data, complemented with expert judgement and risk analyses. This approach has been in place at the ECB for 25 years. It has proven to be a robust way of combining complementary alternative tools that can be flexibly adjusted to address unforeseen events and new challenges. For instance, after the global financial crisis the ECB’s tools were readily extended with non-standard monetary policy measures. The ECB has also adjusted its models, and is continuously improving them, so as to better incorporate climate-related risks. This is to allow the ECB to assess, for example, the effects of acute changes in temperatures or the medium-term effects of carbon taxation. Model revisions and extensions have also been introduced in a timely manner in order to scrutinise the exceptional events and developments unfolding since 2020. These have included epidemiological features during the pandemic and a disaggregation of the energy sector and production structures following the outbreak of Russia’s war against Ukraine. The shocks witnessed in recent years have been unprecedented from a historical perspective, unavoidably leading forecasters across institutions to make larger forecast errors.[7] The ECB will revise its models more extensively if a clear picture emerges as to whether these shocks have fundamentally changed the structure of the economy. Until then, the most robust way to cope with uncertainty remains employing a suite-of-models approach.

As regards the invitation to analyse the supply/demand determinants of inflation, the ECB has been conducting extensive analysis.[8] Studies suggest that the recent surge in inflation was initially mainly driven by supply factors. These notably included developments in energy markets. But other drivers were commodity price developments and the impacts of bottlenecks in global supply chains and pandemic-related shortages of labour. However, over time supply shocks have eased and the relative importance of demand factors has increased. This holds especially for the services sector, where pent-up demand led to strong price increases after the pandemic restrictions were lifted (e.g. in the recreation and travel segments).

2 Financial stability

With respect to the invitation to monitor the situation on non-performing loans (NPLs), the monitoring of bank asset quality is an integral element of the ECB’s regular financial stability assessments. Financial stability is a prerequisite for price stability. In particular, weak asset quality can undermine banks’ intermediation capacity and be detrimental to financial stability. The ECB presents its financial stability assessments in its semi-annual Financial Stability Review, which includes analysis of asset quality developments. The November 2023 issue concludes that higher debt service costs are increasingly posing a challenge to indebted firms, households and sovereigns, although the impact of tighter financial conditions has yet to fully materialise.[9] It notes that banks’ NPL ratios decreased for several years following the establishment of the Single Supervisory Mechanism (SSM). It reports that they stabilised close to multi-year lows in the first half of 2023, with nascent signs of rising losses on some loan portfolios.[10] ECB staff continue to analyse policy developments and put forward advice regarding policies to address NPLs from a macroprudential perspective. This complements the SSM’s work, which takes a microprudential perspective.

3 Climate change considerations in monetary policy

As regards assessing the effects of climate change on its ability to maintain price stability, the ECB continues to integrate climate change considerations into its macroeconomic staff projections and augment its workhorse macroeconomic models to account for mitigation policies. This has helped the ECB to assess different risks. On the one hand, it examines the physical risks of a changing climate and of dwindling ecosystems. On the other hand, it analyses transition risks from moving towards a carbon-neutral economy or from regulatory changes limiting the exploitation of natural resources. Regarding physical risks, the ECB continues to estimate the impact of extreme weather events on inflation.[11] The ECB is deploying innovative modelling techniques to also explore how to incorporate these effects into macroeconomic projections. In addition, the ECB is working on adapting structural models and time series tools to assess the impact of acute and compound physical climate changes on inflation and the real economy. These are to be assessed on an aggregate and a sectoral level. Regarding transition risks, the ECB aims to have state of the art models that analyse the macroeconomic effects of climate change transition policies. For example, such models could measure the impact of green discretionary fiscal policies on growth and inflation in the short term, and the impact of EU policies in the medium term.[12] These kinds of analyses put the ECB in a better position to integrate the impact of climate mitigation policies into staff macroeconomic and fiscal projections, as well as into macroeconomic models. Looking ahead, the new climate and nature plan 2024-2025 sets out the ECB’s efforts to keep exploring other ways in which nature-related risks affect our economy and financial system.[13] This will further contribute to a better understanding of the possible implications for price stability of both climate change and nature degradation.

Regarding the invitation to address market failures while respecting market neutrality, the ECB will continue to adhere to the Treaty principle of “an open market economy with free competition, favouring an efficient allocation of resources”. Market neutrality is an operational tool, rather than a legal requirement. It can help ensure that the ECB’s interventions in the market comply with the open market economy principle. The ECB can justifiably depart from market neutrality in order to comply with the ECB’s objectives and with the relevant Treaty principles. For example, in line with the ECB’s 2021 climate roadmap[14], the Governing Council decided to tilt corporate bond holdings towards issuers with a better climate performance, as of 1 October 2022, through the reinvestment of redemptions. This was necessary to address the carbon bias in the corporate bond portfolio and the resulting accumulation of climate risks in the Eurosystem’s balance sheet. It also enabled the ECB to take its secondary objective into account. The results so far are promising. The weighted average carbon intensity of the ECB’s corporate bond purchase flows decreased by more than 65% in the first year after the implementation of our tilted reinvestments, i.e. from October 2022 to October 2023. The ECB expects the decarbonisation of its corporate sector portfolios to continue throughout 2024 on a trajectory that supports the goals of the Paris Agreement.

Concerning targeted longer-term green refinancing operations or similar instruments: within its mandate, the Governing Council is committed to regularly reviewing its tools in light of its secondary objective, without prejudice to price stability. In its 2021 strategy review the ECB considered refinancing operations with a green target. Such operations would incentivise banks to increase their green lending, for example by offering them an interest rate discount for doing so. However, the review found significant challenges which still persist today. These relate to data coverage and quality, definitions of appropriate green targeting criteria, and verification processes and capabilities. Recent reviews of other measures under the climate and nature plan resulted in a stronger climate tilting for corporate asset purchases. Moreover, they concluded that the valuation haircuts applied to collateral were sufficiently protective against climate-related financial risks.[15] The ECB continues to work on the implementation of a measure to limit the share of assets issued by entities with a high carbon footprint that can be pledged as collateral when banks borrow from the Eurosystem. Furthermore, the ECB will explore – within its mandate – the case for further integrating climate change considerations into monetary policy instruments and portfolios. This commitment is also reflected in the recently agreed changes to our operational framework for implementing monetary policy.[16]

As regards the ECB’s work on climate risk stress tests, the ECB will continue to play an active role in this area. The ECB has further deepened its knowledge of using scenario analysis to assess financial risks arising from climate change. Among other things, the ECB has chaired a workstream on scenario design and analysis within the Network for Greening the Financial System (NGFS).[17] Climate stress tests conducted by the ECB assess resilience to transition and physical risk. These stress tests are carried out for non-financial corporations and euro area banks, as well as the Eurosystem’s own balance sheet. They are based on the combination of projections from the Broad Macroeconomic Projection Exercise (BMPE) and scenarios developed by the NGFS, and apply a range of assumptions in terms of future climate policies. The ECB’s second top-down economy-wide climate stress test showed that acting immediately and decisively would provide significant benefits for the euro area economy and financial system. This would not only maintain the optimal net-zero emissions path, limiting the physical impact of climate change in the long term, but also limit financial risk.[18] In this scenario, financial stability risk would be contained, provided that firms and households could finance their green investments in an orderly manner. In addition, the ECB is now participating, together with the European Supervisory Authorities and the European Systemic Risk Board, in a Fit-for-55 climate stress test exercise. The aim is to assess the resilience of the financial sector in line with the Fit-for-55 package. This one-off exercise is planned to be completed by the first quarter of 2025. It focuses on the EU financial system as a whole and assesses its resilience under a baseline and two adverse scenarios ending in 2030.

With respect to the resolution’s call to address any concerns regarding ideological bias within the ECB, in particular on climate change-related policies, the ECB cherishes diversity of thought, conducts its activities on a factual basis, and will continue to act in line with the competences conferred on it by the Treaties. Diversity and inclusion are deeply embedded in the ECB’s working culture. The ECB is committed to fostering an inclusive work environment free of any form of discrimination. This vision is outlined in the cross-institution diversity and inclusion charter.[19] The charter highlights both the ECB's commitment to promoting working environments based on respect and dignity, as well as the fact that diverse and inclusive workplaces enhance the performance and resilience of organisations. The ECB’s work on monetary policy is driven by its primary objective of price stability. In order to do so, the ECB must take into account climate and nature-related risks to the extent necessary for maintaining price stability and conducting its monetary policy. In addition, under its secondary objective, and without prejudice to its primary objective, the ECB is obliged to support general economic policies in the Union with a view to contributing to the objectives of the Union. The ECB is committed to playing its part within its mandate and according to EU law. The institutions with competence for setting out these general policies have stressed that addressing climate change is a priority also among the Union’s economic policies.

4 Digital euro

With respect to the statement that a digital euro must not replace cash, must respect the privacy of citizens and businesses, and must not endanger financial stability, the ECB reaffirms its commitment to continue to provide cash, while designing a digital euro with a high level of privacy as well as safeguards to protect monetary policy transmission and financial stability. The ECB welcomes the European Commission’s legislative proposals under the Single Currency Package. Once enacted, they would ensure that in an increasingly digitised world, a public payment option would still always be available – in the form of both cash and a digital euro.[20] A digital euro would complement but not replace cash. It would exist alongside cash, in response to people’s growing preference to pay digitally, in a fast and secure way.[21] It would be an electronic form of euro cash, bringing cash-like features to the digital age. It would be designed to provide a level of privacy superior to that of other digital payment methods, and with a number of safeguards to protect monetary policy transmission and financial stability.[22] In particular, digital euro holdings would not be remunerated and there would be limits on the amount of digital euro that could be held by individuals. The ECB will engage with banks and other market participants to define the analytical methodology for determining a holding limit.

Regarding the remark that the introduction of a digital euro depends on a decision of the European Parliament and the Council as co-legislators, the ECB reaffirms that a possible decision by the Governing Council to issue a digital euro would be taken only after adoption of such a legislative act. Broad political support for a digital euro will be crucial for the Eurosystem when deciding whether to issue a digital euro. The ECB is committed to continuing to engage closely with European institutions and authorities on the digital euro project. Opportunities will include its regular public appearances in the Economic and Monetary Affairs Committee of the European Parliament (ECON), also after the legislative deliberations have been concluded. In fact, the Commission proposal on a digital euro stipulates that the ECB would regularly report on the development of a digital euro. Furthermore, the ECB stands ready to provide technical input to support the legislative work and contribute to a timely adoption of the regulation.

5 Crypto-assets and cybersecurity

Concerning the risk of cyberattacks, the ECB points out that it remains very alert with regard to potential cyberattacks, closely monitoring possible threats and adjusting its protection measures where needed, in close cooperation with European System of Central Banks and SSM institutions, as well as the other EU institutions, bodies and agencies. As regards the TARGET[23] Services – which ensure the free flow of cash, securities and collateral across Europe – the national central banks (NCBs) providing these services remain vigilant regarding their security and resilience. They closely monitor and follow up on any threats that occur. Strong cybersecurity measures have been put in place and are regularly reviewed. Whenever necessary, additional measures are decided on in order to adequately protect the systems. Under the Eurosystem Cyber Resilience Strategy for financial market infrastructures (FMIs), the ECB – together with the euro area NCBs – has established multiple initiatives. These aim to heighten entities’ cyber resilience, with the central banks acting either in an overseer capacity or as a catalyst. For example, the ECB coordinated and applied the TIBER-EU framework[24], allowing for advanced, in-depth testing in a controlled manner. Moreover, the ECB assessed the entities it oversees against a set of requirements so as to continuously improve their cyber resilience postures. To catalyse public-private initiatives on strategic cyber topics, the ECB chaired the Euro Cyber Resilience Board (ECRB), a forum for discussions between pan-European FMIs, their critical service providers and public authorities. The ECRB established the Cyber Information and Intelligence Sharing Initiative to share cyber intelligence and exchange best practices. The ECB has also participated in discussions with other policymakers at EU and international level.

With regard to the monitoring of new types of digital assets, such as crypto-assets, and the related risks in terms of cybersecurity, money laundering, tax fraud, terrorist financing and other criminal activities related to the anonymity provided by crypto-assets, the ECB continues to closely monitor developments in the crypto-asset ecosystem and assess related risks. The ECB continues to be outspoken about the risks of crypto-assets and ECB staff have contributed to technical policy discussions on how to monitor such risks.[25] In addition, the ECB has contributed to the monitoring and analysis of risks from crypto-assets at the EU and international levels.[26] As part of its oversight function the ECB oversees and monitors payment schemes and arrangements, and regularly monitors relevant activities in crypto-assets. Such monitoring includes digital payment tokens that have reached a certain level of significance for the euro area. It is also helping the European Supervisory Authorities prepare regulatory technical standards to operationalise the new bespoke regime for markets in crypto-assets under the proposed Markets in Crypto-Assets (MiCA) Regulation. The ECB closely followed the finalisation of the new EU anti-money laundering/countering the financing of terrorism (AML/CFT) framework. It looks forward to welcoming and establishing close cooperation with the new AML Authority (AMLA) in Frankfurt. The ECB has also continued to closely monitor discussions on the regulation of virtual assets in the Financial Action Task Force. Finally, the ECB participates in various international standard-setting bodies. In this way it continues to help develop international standards to address the risks of crypto-assets and their service providers, including the risks arising from their links to the financial sector.

6 Accountability, transparency, and other aspects

As regards the resolution’s emphasis on maintaining the ECB’s accountability and transparency towards the European Parliament, the ECB places great importance on its accountability relationship with the European Parliament and intends to continue publishing a written feedback statement as part of its resolution on the ECB Annual Report. The relationship of accountability with the European Parliament has evolved over time in response to demands for enhanced accountability and transparency. The ECB is committed to continuously refining these frameworks to ensure they remain effective and fit for purpose. In demonstration of the constructive relationship between the institutions, the ECB and the Parliament in 2023 signed an exchange of letters structuring their interaction practices in the area of central banking.[27] As part of these arrangements, the ECB intends to continue providing detailed feedback on Parliament’s resolution on the ECB’s Annual Report of the previous year. The feedback is published on the ECB’s website together with its Annual Report. This underscores the Bank’s accountability and transparency efforts. In general, it not only appreciates the scrutiny, but also the insights gained through interactions with the European Parliament. Additionally, the ECB welcomes these opportunities to explain ECB policies to elected representatives and citizens more effectively. The ECB will continue to address such scrutiny requests from the European Parliament and will strive to enhance the interactions with its Members of Parliament, in accordance with the provisions of EU primary law.

Regarding the request to devote a chapter in the ECB Annual Report to explaining how the ECB has interpreted and acted upon its secondary objective, the ECB notes that its Annual Report 2023 includes a dedicated box explaining how the secondary objective is considered in the conduct of the ECB’s monetary policy and reporting activities. Without prejudice to price stability, the Governing Council caters for considerations related to the secondary objective in its monetary policy decisions. The secondary objective is explicitly recognised in the ECB’s monetary policy strategy. This was noted also in the feedback statement to the European Parliament’s resolution on the ECB Annual Report 2021. Provided that two configurations of the instrument set are equally conducive and not prejudicial to price stability, the Governing Council, when adjusting its monetary policy instruments, chooses the configuration that best supports the general economic policies in the Union related to growth, employment and social inclusion and that, with a view to contributing to the Union’s broader objectives, protects financial stability and helps to mitigate the impact of climate change. The box in the Annual Report 2023 describes in more detail how the ECB communicates about its actions on the secondary objective. This topic is addressed in the Bank’s press conferences, accounts of monetary policy meetings and various other publications. Lastly, the box elaborates on where in the Annual Report to find the reporting on monetary policy decisions and the underlying analyses of relevance to the secondary objective.

As regards the statement on taking better account of and respecting the European Parliament's prerogatives in future appointment procedures, in particular in relation to the SSM, the ECB reaffirms that it attaches great importance to the European Parliament’s views and fully respects its role in the appointment procedure. The selection process for the Chair of the ECB Supervisory Board was rigorous and transparent, in full respect of all relevant provisions. Accordingly, the ECB proposed a final candidate and the European Parliament decided to approve the candidate. The process is set out in the SSM Regulation[28], the inter-institutional agreement between the European Parliament and the European Central Bank on the practical modalities of the exercise of democratic accountability and oversight over the exercise of the tasks conferred on the ECB within the framework of the SSM[29] and in the Memorandum of Understanding between the Council of the European Union and the ECB on the cooperation on procedures related to the SSM[30].

As regards the invitation to further enhance its communication about central bank policy objectives and crisis responses, the ECB seeks to continuously innovate and adapt its communication to a changing media and communications landscape to make sure its messages are conveyed effectively. Especially at a time when higher prices are a key concern for Europeans, the ECB is seeking to connect with audiences beyond expert circles. The Bank has been communicating through a variety of new formats to re-emphasise its core goal of bringing inflation back down. Recent data – for instance from the ECB’s Consumer Expectations Survey – confirm that television, radio and other general interest media continue be important channels for achieving this.[31] ECB representatives are therefore continuing their efforts to be present in those media and elsewhere. For instance, the novel ECB & You format explains ECB policy, how the Bank has responded to the recent inflation surge and the reasons behind its decisions. We are committed to reaching the wider public and helping build knowledge and understanding of the ECB’s policies and objectives. Particularly in times of crises, such outreach remains a core element of making monetary policy more effective and fostering trust in the central bank.

With respect to the suggestion to create an internal evaluation office for ex post assessment of its policy decisions, the ECB is committed to the highest standards of policymaking and conducts wide-ranging evaluations of its own analysis and decisions. The ECB engages in targeted reviews of its policies on an ongoing basis. For example, on 13 March 2024 the Governing Council concluded a review of the operational framework for steering short-term interest rates.[32] Moreover, the ECB conducted strategy reviews in 2003 and again in 2020-21. These reviews involved a broad cross-section of the organisation in evaluating the performance of its monetary policy strategy. Furthermore, in 2020-21 the public was also involved. As announced in 2021, going forward the ECB intends to conduct reviews of its monetary policy strategy periodically. The next assessment is expected in 2025. In addition, the ECB is subject to a wide range of external and ad hoc or systematic ex post evaluations by academics, non-governmental organisations and other entities. The design and conduct of monetary policy are hence constantly debated and discussed. They are evaluated in academic papers, including those prepared prior to the regular monetary dialogues in the ECON Committee. They are also debated at conferences arranged both by the ECB and external parties. The ECB will continue to reflect on how to improve the ex post evaluation of its policies. It aims to ensure that they are in line with best practices in the central banking community.

Regarding the call to look into strengthening the international role of the euro with a view to raising its attractiveness as a reserve currency, the ECB reaffirms that the international role of the euro is primarily supported by a deeper and more complete Economic and Monetary Union (EMU), including advancing the capital markets union and completing the banking union, in the context of the pursuit of sound economic and fiscal policies in the euro area. The ECB emphasises the need for further efforts to complete EMU, and supports these policies. Further advancing European economic and financial integration is a responsibility of the co-legislators. It will be crucial to enhancing the resilience of the euro's international role in a potentially more fragmented global economy. Strong economic fundamentals, including sustainable debt levels, are important determinants of international currencies. The global appeal of a currency depends crucially on predictability and stability. At the same time, inflation also matters for international currency status. The ECB remains committed to maintaining price stability in the medium term. It will continue to monitor the international role of the euro and publish its analysis in the related reports.[33]

7 ECB institutional matters

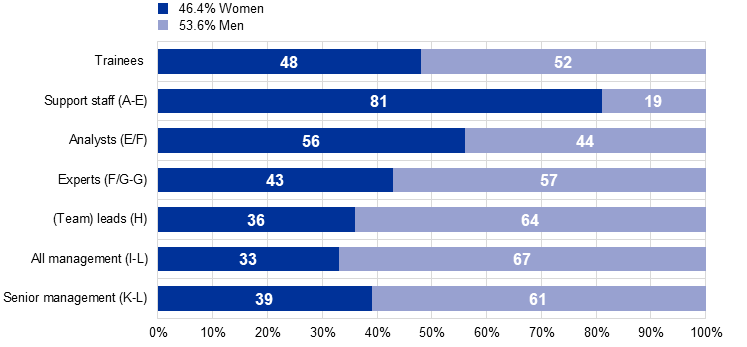

In response to the invitation to continue its work to strengthen equal opportunities for all genders in its organisation, the ECB highlights its commitment to improving and sustaining greater gender balance across the bank, while at the same time embracing diversity and inclusion in their full spectrum. In recent years the ECB has kept its strategic focus on gender diversity, through a dedicated 2020-26 gender strategy with gender targets until 2026.[34] At the end of December 2023 the composition of the ECB workforce by gender remained relatively balanced, with 46% of employees being women and 54% men. The share of women had reached 39% in senior management and 33% across all management. This is particularly important for creating role models and mentoring opportunities. The gender gap at expert and team lead levels remained challenging, with only 43% and 36% of such positions, respectively, held by women. At analyst level, the share of women has continued to grow and 56% of such positions were held by women. This further increased the pool of female talent eligible for career progression. A number of measures have been implemented to ensure equal opportunities for all genders and many other dimensions of the human identity. These measures include inclusive job descriptions, diverse recruitment panels, targeted outreach to under-represented talent at dedicated career fairs,[35] a dedicated scholarship for women, and the Women’s Leadership Programme. In addition, the ECB offers mentoring programmes with the option to select a focus on certain diversity dimensions, flexible working arrangements, accessibility and reasonable accommodations for colleagues with different abilities. To further develop and implement these measures, the ECB and its human resources department are partnering with diversity ambassadors from various business areas and an employee-led diversity network. The ECB will continue implementing its gender diversity strategy while embracing diversity and inclusion from an all-round perspective. In doing so, it aims to empower every colleague to bring their full potential to work.

Chart 1

Our employees and trainees by gender

(percentages of workforce by salary band)

Source: ECB data as of 31 December 2023 for permanent staff members and staff with fixed-term contracts.

As regards the invitation to regularly re-examine its ethics framework, the ECB confirms that this is its practice. It recalls that, following the enhancement of the Ethics Guidelines for the Eurosystem and the SSM[36], the ethics framework for ECB staff is currently being reviewed. This review aims at bringing the ECB’s rules for staff in line with the latest standards for conduct and integrity, as included in the above Guidelines. Once the ongoing review of the ethics framework for ECB staff has been completed, the ECB will inform the European Parliament of its outcome. The ECB notes that since 1 January 2023 high-level ECB officials have been subject to enhanced rules for private financial transactions.[37] The new rules significantly improve on the previous regime by providing additional safeguards and introducing regular compliance monitoring. Accordingly, they ensure that the ECB will remain among the leading institutions for good conduct and integrity within Europe and internationally.

Concerning the resolution’s call for the ECB to bring its internal whistleblowing framework into line with the EU Whistleblower Directive, the ECB notes that the Directive is addressed to the EU Member States and should apply where officials and other servants of the Union report breaches that occur in a work-related context, outside their employment relationship with the Union institutions, bodies, offices or agencies.[38] Nonetheless, as previously stated[39], the ECB’s framework[40] is fully aligned with the principles of the Directive. It provides both a user-friendly tool, allowing anonymous reporting, as well as strong rules to protect whistleblowers against retaliation. In the course of 2023 – the tool’s third full year in operation – it was used to report more than half the whistleblowing cases in the ECB, mostly on an anonymous basis.

The text of the resolution as adopted is available on the European Parliament’s website.

The cut-off date for the preparation of this feedback statement was 27 March 2024.

See “Estimates of the natural interest rate for the euro area: an update”, Economic Bulletin, Issue 1, ECB, 2024.

See “Feedback on the input provided by the European Parliament as part of its resolution on the ECB’s Annual Report 2021”.

See “An overview of the ECB’s monetary policy strategy” on our website.

See ECB staff analyses, for example, Ciccarelli et al., The ECB Blog, ECB, 5 July 2023 and Ciccarelli et al., Occasional Paper Series, No 344, ECB, 2024, for a recent review of how the ECB utilises macroeconomic models to perform economic projections.

For a discussion of the performance of recent ECB projections, please see “What explains recent errors in the inflation projections of Eurosystem and ECB staff?”, Economic Bulletin, Issue 3, ECB, 2022.

See “The role of demand and supply in underlying inflation – decomposing HICPX inflation into components”, Economic Bulletin, Issue 7, ECB, 2022.

See “Financial Stability Review”, ECB, November 2023.

Bank asset quality is also an important topic for ECB Banking Supervision. See the ECB’s reply to the European Parliament’s “Resolution on Banking Union – Annual Report 2023” for a detailed summary of supervisory initiatives undertaken by the ECB in this field.

An ECB staff research study, for example, found that the extreme summer heat of 2022 increased euro area food price inflation by 0.8% after 12 months. See Kotz, M., Kuik, F., Lis, E., and Nickel, C., “The impact of global warming on inflation: averages, seasonality and extremes”, Working Paper Series, No 2821, ECB, May 2023.

A special feature on macroeconomic effects of climate change transition policies, including an assessment of the impact of green discretionary fiscal policies on GDP growth and inflation was published in early 2024. See “Assessing the macroeconomic effects of climate change transition policies”, Economic Bulletin, Issue 1, Section 4, ECB, 2024.

See “Climate and nature plan 2024-2025 at a glance”.

See “ECB presents action plan to include climate change considerations in its monetary policy strategy”, press release, ECB, 8 July 2021.

For more information on this decision on collateral haircuts, see “Decisions taken by the Governing Council”, ECB, October 2023.

See “Changes to the operational framework for implementing monetary policy”, Statement by the Governing Council, ECB, 13 March 2024.

The NGFS workstream on scenario design and analysis produces widely recognised climate scenarios, used by central banks, supervisors and the financial sector. In parallel with the updates of long-term scenarios, the NGFS has started to develop short-term scenarios. These will focus on potentially severe near-term climate-related risks and can be used for climate stress tests and similar exercises.

See “Faster green transition would benefit firms, households and banks, ECB economy-wide climate stress test finds”, press release, ECB, 6 September 2023.

In 2022 the ECB launched a cross-institutional charter on equality, diversity and inclusion in collaboration with other institutions from the European System of Central Banks (ESCB) and the Single Supervisory Mechanism (SSM). See “ECB launches equality, diversity and inclusion charter”, press release, ECB, 26 July 2022.

See “Proposal for a Regulation of the European Parliament and of the Council on the establishment of the digital euro”, European Commission, COM/2023/369 final, 28 June 2023; “Proposal for a Regulation of the European Parliament and of the Council on the legal tender of euro banknotes and coins”, European Commission, COM/2023/364 final, 28 June 2023; and “ECB welcomes European Commission legislative proposals on digital euro and cash”, press release, ECB, 28 June 2023.

The Eurosystem’s cash strategy aims to ensure that cash remains widely available and accepted as both a means of payment and a store of value.

For more information on the progress of the digital euro project, see the report “A stocktake on the digital euro”, ECB, 18 October 2023 and “Preserving people’s freedom to use a public means of payment: insights into the digital euro preparation phase”, introductory statement by Piero Cipollone at the Committee on Economic and Monetary Affairs of the European Parliament, Brussels, 14 February. In addition, see “Opinion of the European Central Bank of 31 October 2023 on the digital euro (CON/2023/34)” (OJ C, C/2024/669, 12.1.2024).

Services developed and operated by the Eurosystem which ensure the free flow of cash, securities and collateral across Europe.

TIBER-EU is a European framework for threat intelligence-based ethical red-teaming. It provides comprehensive guidance on how authorities, entities, and threat intelligence and red-team providers should work together to test and improve the cyber resilience of entities by carrying out controlled cyberattacks. See “What is TIBER-EU?”.

ECB staff presented a note to the 2023 IMF statistical forum on the ECB’s crypto-asset dataset and the indicators that it uses for the regular monitoring of crypto-asset activities and major crypto players. See also “Paradise lost? How crypto failed to deliver on its promises and what to do about it”, speech by Fabio Panetta at the 22nd BIS Annual Conference, 23 June 2023, for further references to ECB crypto-asset monitoring data.

Examples include “Crypto-assets and decentralised finance”, ESRB, 2023, the “EU Non-bank Financial Intermediation Risk Monitor 2023”, ESRB, 2023, “The Financial Stability Risks of Decentralised Finance”, Financial Stability Board (FSB), 2023 and “The Financial Stability Implications of Multifunction Crypto-asset Intermediaries”, FSB, 2023.

See “Exchange of Letters between the ECB and the European Parliament on structuring their interaction practices in the area of central banking” on the ECB’s website.

See Council Regulation (EU) No 1024/2013 of 15 October 2013 conferring specific tasks on the European Central Bank concerning policies relating to the prudential supervision of credit institutions (OJ L 287, 29.10.2013, p. 63).

See the Interinstitutional Agreement between the European Parliament and the European Central Bank on the practical modalities of the exercise of democratic accountability and oversight over the exercise of the tasks conferred on the ECB within the framework of the Single Supervisory Mechanism (OJ L 320, 30.11.2013, p. 1).

See the Memorandum of Understanding between the Council of the European Union and the ECB on the cooperation on procedures related to the Single Supervisory Mechanism (MOU/2013/12111).

See for example “Credibility gains from communicating with the public: evidence from the ECB’s new monetary policy strategy”, Working Paper Series, No 2785, ECB, February 2023.

See “ECB announces changes to the operational framework for implementing monetary policy”, press release, ECB, 13 March 2024.

See “The international role of the euro”, ECB, June 2023.

See “ECB announces new measures to increase share of female staff members”, press release, ECB, 14 May 2020.

See “Diversity Networks” on the ECB website.

See Guideline (EU) [2021/2253] of the European Central Bank of 2 November 2021 laying down the principles of the Eurosystem Ethics Framework (ECB/2021/49), (OJ L 454, 17.12.2021, p. 7) and Guideline (EU) 2021/2256 of the European Central Bank of 2 November 2021 laying down the principles of the Ethics Framework for the Single Supervisory Mechanism (ECB/2021/50) (recast), (OJ L 454, 17.12.2021, p. 21).

See “ECB publishes enhanced rules for private financial transactions of high-level officials”, press release, ECB, 16 December 2022.

See recital 23 of Directive (EU) 2019/1937 of the European Parliament and of the Council on the protection of persons who report breaches of Union law (OJ L 305, 26.11.2019, p. 17).

See “Feedback on the input provided by the European Parliament as part of its resolution on the ECB’s Annual Report 2021”.

See Decision of the European Central Bank of 20 October 2020 amending the European Central Bank Staff Rules as regards the introduction of a whistleblowing tool and enhancements to the whistleblower protection (ECB/2020/NP37) and Decision (EU) 2020/1575 of the European Central Bank of 27 October 2020 as regards the assessment of and follow-up on information on breaches reported through the whistleblowing tool where a person concerned is a high-level ECB official (ECB/2020/54), (OJ L 359, 29.10.2020, p. 14).

| Zařazeno | čt 18.04.2024 09:04:00 |

|---|---|

| Zdroj | ECB Publication |

| Originál | ecb.europa.eu//press/pubbydate/2024/html/ecb.20240418_feedback_on_the_input_provided_by_the_european... |

RSS - všechny zprávy

RSS - všechny zprávy Vložit zprávy na www stránky

Vložit zprávy na www stránky